How often have you quoted a job but ended up losing on it because the hours blew out? It happens to everyone once in a while… but get this wrong too often, and you won’t be very profitable.

Even the big players in our industry get this wrong more than they’d like to admit… Fletcher’s got in trouble last year with overruns on a number of their major projects. It cost them millions.

Did you know: the Sydney Opera House was completed a massive 10 years behind schedule?!

Clearly, when you want to make money on your jobs, it’s very important to accurately estimate how much time they will take. If you’ve ever wondered why your quotes don’t work out, this is a good starting point.

Research shows only 17% of the population can accurately estimate how much time a job or task will take. Basically, we’re all optimists. We tend to believe the future will be better than the past.

If only 17% can estimate time correctly, that means 83% are getting it wrong. Mistakes include:

- Failing to consider how long it’s taken us to complete similar tasks in the past (science calls this the planning fallacy)

- Assuming that we won’t run into any complications that will cause delays (science calls this an optimism bias)

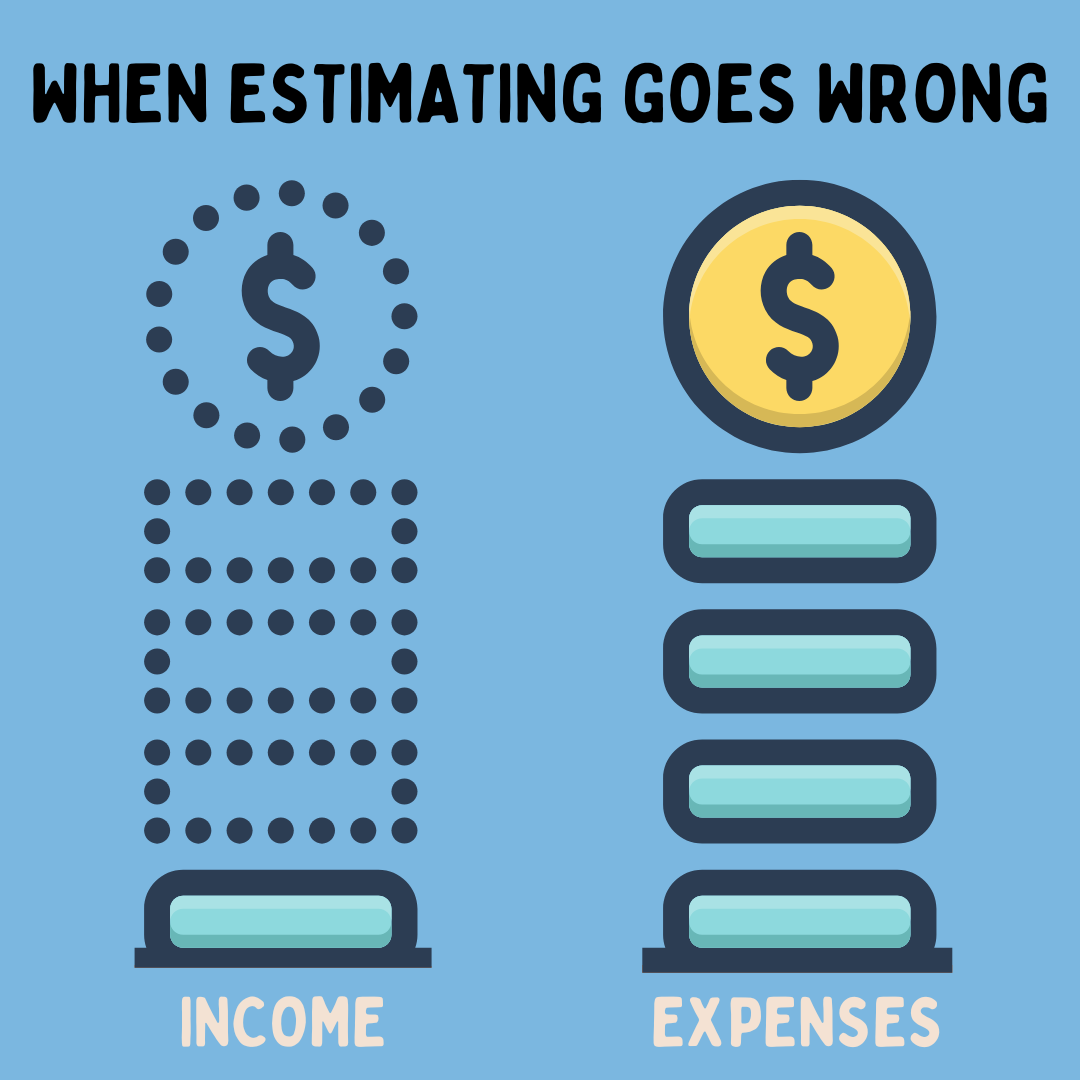

There are a lot of moving parts in a business, and if you often underestimate hours on jobs, or don’t allow for unexpected curveballs, you won’t make the margin you need to.

Achieving target margins consistently on every job is key when it comes to being profitable. Let’s not forget: when costs exceed what you quoted, that cold hard cash comes directly out of your pocket.

In very real terms, that means less income for you, and stressful cashflow. And that is all kinds of bad, especially for a family business. Plus, cashflow headaches are the #1 reason for going broke.

So how can the average tradie business owner override their planning fallacy and optimism bias?

The secret is to be dealing with concrete numbers. They make things very black and white, allowing for smarter decision-making. That’s the kind of strategic thinking required for both quick wins and long-term success.

I’ve worked with hundreds of tradie businesses, and I can tell you: it’s amazing the insights you can get from a simple deep dive into the numbers – when you know what to look for (most don’t).

Yes, one important part of this is back-costing (checking all costs – including time/labour – on previous jobs to see how your quote stacked up against what actually happened).

To do this, you first need to be working with the right project management software, time-tracking app or system for your specific business. Then, the main thing is, use a structure – so back-costing is easy and doesn’t take all day! It is especially important if you run multiple jobs and have a large team.

Revisit regularly and make sure you are charging enough. The trick is to then actually deploy this historical data and turn it into increased accuracy on your next job.

When I assist clients in the business coaching process to really look at their previous jobs, they can see exactly where they’re losing money on under-quoting. From then on, everything becomes much easier.

Be sure to use a pricing formula, so you have certainty that your price is fair. Not too low that you won’t make money. Not too high that you’ll be priced out (or if you are, you can walk away confident, knowing the margin was not enough – you don’t work for free).

Using a formula also means you price consistently regardless of whether you’re feeling optimistic, tired, are desperate for work for your team, or have too much on already.

Include your ‘fudge ratio’ calculation and buffer percentage to build in extra hours for delivery delays, staff absences, weather, etc.

Finally, you need a strong gross profit margin

A ‘good’ margin to add on top varies for each company, depending on your overheads and industry. So it’s important to know what is a good margin percentage to be aiming at in your market.

Although, if it’s not at least 20%, I’d encourage you to make some adjustments right away. Anything under this, and you won’t be able to cover overheads and still make the profits you need to maintain a successful business.

Studies also show that while we are generally bad at estimating how long it takes us to do the job, we’re quite good at estimating how much time the job will take when others are doing the work. So, harnessing the talents and objectivity of someone outside your immediate team (like a QS) could be a smart move.

Ultimately, accurate predictions and back-costing effectively ensures you will achieve the target margins you need, become more profitable, and grow safely, even with the variables and any bias you may have.

Tweaks like this in profitability and productivity typically get my clients return-on-investment far exceeding costs inside 3-6 months.

Book a time with me here to find out how I might be able to help you:

nextleveltradie.co.nz/nextstep/

Daniel Fitzpatrick

![]()

Published in WIRED issue 75/December 2024 by Fencing Contractors Association NZ

You may also like: 4 mindsets that separate successful business owners from the rest

Read WIRED online

Follow us on Facebook

© Fencing Contractors Association NZ (FCANZ)